Investment Academy ETFobchodník

14 lessons that will teach you how to invest successfully and build your wealth

0 of 13 lessons completed

COURSE CONTENT

What is investing?

People imagine complicated graphs, wolves of Wall Street, or gambling when it comes to investing.

Investing is not a luxury reserved for the wealthy, but a basic tool for anyone who does not want their lifelong work to depreciate over time.

It is a conscious decision: Today, instead of immediate consumption (buying a new phone or clothes), you put your resources into something that has the potential to grow. Your money thus becomes your employee. While you sleep, relax, or work, your invested euros work in the background to build your future freedom.

The goal of investing is the efficient use of available financial resources. Investments serve not only to increase savings but also to build a reserve for the future.

Active vs. Passive: Which way are your money flowing?

In order to invest successfully, you need to understand one fundamental difference. It's not about how much money you make, but about where you put it.

- Asset: Something that brings you additional money.

- Liability: Something that only consumes money.

ACTIVITIES (Puts money in the pocket)

- Stocks and ETF funds (increase in value and pay dividends)

- Real estate for rent (rental income from tenants)

- Education and courses (increase your market value)

- Entrepreneurship (profits from selling products/services)

- Bonds (regularly paid interest/coupon)

PASSIVE (Money is taken out of the pocket)

- Consumer loan and leasing (interest you pay to the bank)

- Own housing (mortgage, utilities, repairs)

- Latest electronics (loses value immediately after purchase)

- Expensive hobbies and subscriptions you don't use

- Car for personal use (fuel, service, insurance)

Saving vs. Investing

SAVINGS (Essence, but loss of value)

- • Low interest rates (0.1% - 2%)

- • Loss of purchasing power due to inflation

- • Suitable only for short-term goals

- • Emergency fund (3 - 6 months of expenses)

Goal: Short-term reserve for unexpected expenses (car repair, washing machine)

Where: Current account, savings sub-account, money "under the mattress"

Interest: Almost zero, your money in the bank "sleeps"

Inflation: Is your enemy, every year you buy less for the same money

Availability: You have immediate access to the money (high liquidity)

INVESTING (Risk, but growth of wealth)

- • Higher yields (5% - 10% + annually)

- • Protection against inflation

- • Suitable for long-term goals (5+ years)

- • Wealth building over time

Goal: Long-term asset building (retirement, early freedom)

Where: Stocks, ETF funds, bonds, real estate

Return: Historically averaging 7 - 10% per year (in stock index)

Inflation: Is beaten by market growth, your purchasing power is increasing

Availability: Requires time (horizon 5+ years) for the best result

Saving in a current account may seem safe, but in terms of building wealth, it is a "guaranteed path to loss of purchasing power." Your thousand in the bank will still be a thousand in ten years, but the shopping basket you fill with it will be a third smaller.

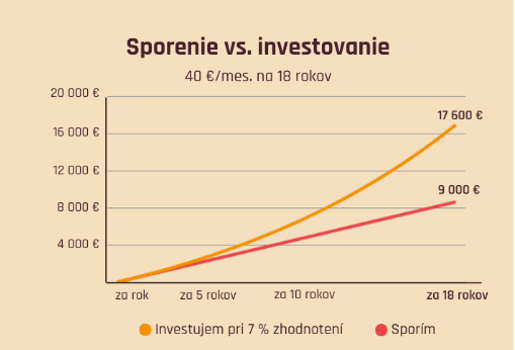

*example with an average annual return of 7%

1. Investing with a 7% return

regular monthly deposit of €40,

average annual appreciation of 7%.

The curve has an exponential shape, which means that the money does not start growing linearly, but the growth rate gradually accelerates. At the end of the 18th year, the invested amount reaches approximately €17,600, clearly demonstrating the effect of compound interest.

2. Savings without appreciation

without interest,

without investing,

just regular money deposits.

Example: Saving vs. Investing

With a regular monthly deposit of €40 over 18 years:

How did it all start, actually?

History of investing

The emergence and history of investing (key moments)

First forms

Investing did not start with money, but with loans of seeds or livestock that brought a harvest or offspring.

Ancient and medieval

The foundations were laid by the first merchants who financed ships and caravans in the hope of higher profits from the sale of goods.

17th century (1602)

The Dutch East India Company was established, which was the first to issue shares to the public, considered the birth of the modern stock exchange.

18th century (around 1774)

Adriaan van Ketwich in the Netherlands created the first investment fund with the idea of risk diversification (investment distribution).

19th century

The expansion of mutual funds and the first ETF funds (1993), which simplified access to investing for ordinary people.

Slovak specificity

Inflation - the silent thief

Imagine you have a 500-euro banknote tucked away in a drawer. A year later, you pull it out and even though the number on it remains the same, you suddenly realize that you can buy three loaves of bread less for it in the store. That's not magic, that's inflation in practice.

Inflation is the widespread increase in prices of goods and services that subtly, but persistently, erodes your savings.

What is it actually?

Inflation is the general increase in prices of goods and services over time. It doesn't just mean that butter or gasoline has become more expensive. It means that the purchasing power of your currency is decreasing. For the same amount of money, you simply can afford less. That's inflation - the silent enemy of your savings.

Why inflation is eating up your savings

With 3% inflation, you will lose approximately 25% of purchasing power in 10 years. This means that €10,000 in the account will only have a real value of €7,500.

Why does it actually arise?

Economists distinguish two main engines of inflation:

1. More money in circulation

2. Expensive inputs

How to defend against it?

The only effective defense is to invest in assets that historically beat inflation (e.g. stock markets averaging 7 - 10% per year). Your goal is not just to have "more money," but to preserve and increase its real purchasing power.

Is inflation always just the "bad cop"?

What is considered "healthy" inflation?

The ideal state is considered to be a stable level of approximately 2% per year.

This number is not random. It is the official target of most of the world's most important central banks, such as the European Central Bank (ECB) or the Federal Reserve (FED).

- If it is too low: The economy freezes and recession looms.

- If it is too high: People lose certainty, prices soar, and savings evaporate too quickly.

Basic investment tools

When you decide to invest, you are basically choosing a "vehicle" that will take you to your financial goal. Each vehicle has a different speed (return) and a different level of comfort or risk (stability).

Stock market: Engine of growth

Stocks represent ownership in real companies. When you own shares of Apple or Microsoft, you become a partner of these technological giants. If companies innovate and make profits, you benefit from the growth in their stock prices or from the dividends paid out.

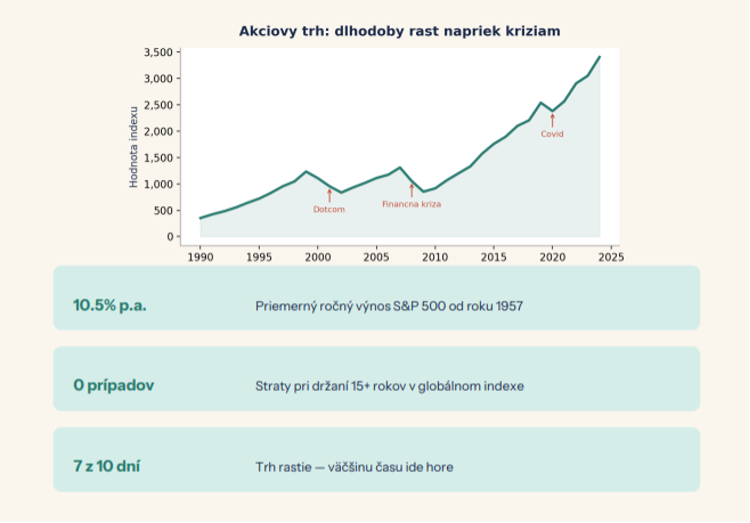

The stock market is historically the most performing asset class. Despite wars, pandemics, or crises, the market has always recovered and reached new highs. The key to success is patience - those who invested in a global index* and held for at least 15 years have never been at a loss in history.

*An index itself is not a product that you can buy. It is just a statistical indicator or a list of securities that tracks the performance of a specific market or sector.

Bonds: Anchor portfolios

A bond is essentially a debt note. When you buy a government bond, you are lending money to the state (e.g. Slovakia or the USA). In return, the state promises to pay you interest regularly and return the full amount at the end. Bonds are usually less volatile than stocks. When markets are falling, bonds tend to keep your investment afloat.

ETF: The best choice for a beginner

Imagine ETF as a shopping basket. Instead of spending hundreds of hours analyzing one company, you buy the whole basket, which includes, for example, the 500 largest companies in the world.

- Diversification: If one company in the basket goes bankrupt, you have 499 others to replace it. The risk of losing all your money is almost zero with broad ETFs.

- Low costs: ETFs do not require expensive managers in suits, so fees are minimal, which will save you thousands of euros in the long term.

An ideal example is the historical development of the S&P 500 index:

* Notice those "teeth" on the graph - those are crises (e.g. 2000, 2008, or 2020). Each fall was ultimately just a small deviation on the way up. *Maintain in mind that the presented data depict past developments and are not a reliable indicator of future trends.

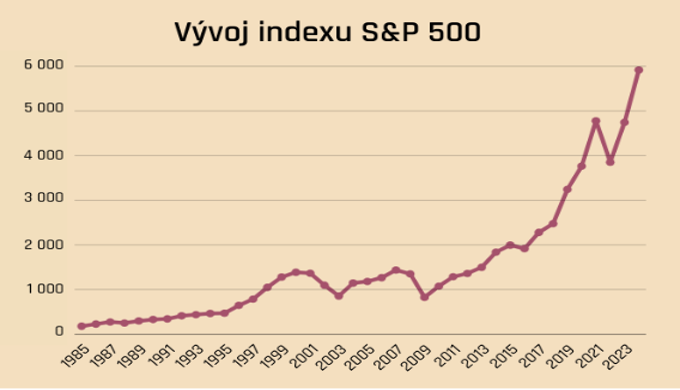

What does the history of the S&P 500 index tell us?

The S&P 500 index, which tracks the 500 largest and most successful companies in the USA, is considered the best barometer of the global stock market.

- • Original value: When the index was created in 1957, its value was approximately 44 points.

- • Today's value: Today it is moving at levels exceeding 6,000 points.

- • Average yield: Historically, this index delivers an average annual return of approximately 10% p.a. (before accounting for inflation).

| Tool | Main BENEFITS | MAIN RISKS | For whom |

|---|---|---|---|

| Action (Share in the company) |

|

|

Long-term investor (10+ years) |

| Bond (Loan to a company/state) |

|

|

Conservative investor (3-5 years) |

| ETF (Index fund) |

|

|

Ideal base for 95% beginners |

Why invest at all?

Protection against inflation

Money in a current account loses value. Investing allows you to achieve a return higher than the inflation rate, thus preserving the purchasing power of your savings.

Financial independence and retirement

Investing is an effective way to build up a sufficient financial reserve for retirement, as state pension systems are unsustainable in the long run.

Achieving financial goals

Investing helps with long-term goals such as buying real estate, educating children, or retiring early.

Regularity reduces risk

Regular investing (e.g. monthly) averages the purchase price, so you don't have to worry about whether you are investing at the right time.

History plays in favor of long-term investors

Despite short-term declines, stock markets have been growing in the long term, and each crisis so far has presented an opportunity for higher future returns.

Asset Evaluation (Compound Interest)

The sooner you start, the longer your money has to grow. Compound interest means that you are not only increasing the original deposit, but also the interest already earned, leading to exponential growth.

The Miracle of Compound Interest

"Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it." — A. Einstein

Your interests earn additional interests. It's like a snowball rolling over time. The sooner you start, the more dramatic the effect. The difference between saving and investing is huge after 30 years.

Comparison of time horizons (monthly deposit 20 €)

We still see a relatively large share of your deposits. The interests are already working, but the snowball is just starting to roll.

The card is turning here. The evaluation is already greater than the amount you have deposited into the system yourself. Your money is starting to earn more than you.

This is the moment of "magic". Although you only invested €2,400 more than in the 30th year, the total amount has almost doubled.

Risk vs Return

When looking for a place for your money, you probably desire a combination that everyone wants: high profit, zero risk, and money available anytime. However, in the world of finance, a harsh truth applies - such a product does not exist. You have to set your priorities.

These three key pillars define this relationship:

Yield

How much money will your investment earn you

Security

What is the probability that you will not lose money

Availability (Liquidity)

How quickly can you convert an investment back into cash

Basic rule of investing

Higher returns = higher risk. There is no investment with high returns and zero risk. If someone promises you the opposite, it's a scam.

Investment risks

- Short-term market fluctuations (portfolio value may temporarily drop by 20-40%)

- Emotional reactions and panic during declines

- Low-quality or risky projects (especially in the cryptocurrency area)

- Insufficient diversification - too much dependence on one company or one type of asset

| Asset type | Profit potential | Risk level | Availability of money | Fatigue |

|---|---|---|---|---|

| Cash at home | Zero | Low | Immediate | Profitability |

| Regular account | Negligible | Low | Immediate | Profitability |

| Savings product / Term deposit | Low | Low | Limited | Availability |

| Government securities | Conservative | Very low | High | Profitability |

| Stock indexes (ETFs) | Tall | Medium to high | High | Security |

| Corporate bonds | Middle | According to the company's credit rating | Central | Security |

| Investment apartments and houses | Medium to high | Central | Low | Availability |

| Alternatives (Crypto, Gold) | Speculative | Very high | High | Security |

Diversification

Portfolio diversification is an investment strategy aimed at minimizing risk by spreading capital among different types of assets. It operates on the principle of "not putting all your eggs in one basket," thus protecting the investor from significant loss in the event of a decline in a specific investment.

WHY DIVERSIFY?

Risk reduction

If one action falls, the others will compensate for it.

Yield stability

Portfolio has a smoother growth without dramatic fluctuations

Better sleep

You don't have to follow every news about one company

Beware of the illusion of diversification!

If you own shares of Apple, Microsoft, and Nvidia, you are not diversified. All these companies are from the same sector (technology) and the same country (USA).

Real diversification means that if the technology sector falls, you will be supported by companies producing food, drugs, or government bonds, for example.

100% investment from one Slovak bank

Risk: Extremely high

500 companies across the USA, Europe, and Asia + bonds

Risk: Medium to low

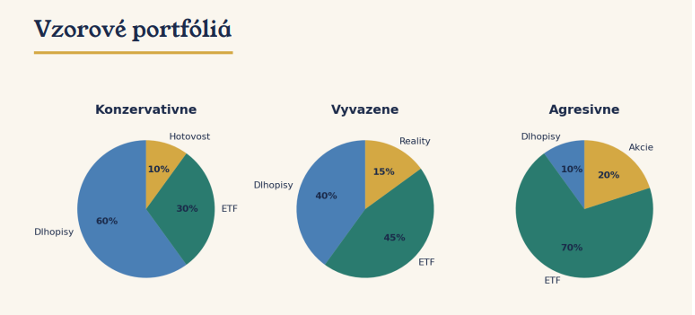

How to diversify properly:

There are several classes of assets that you can use to build a portfolio. Each has a different risk-return ratio. Diversification is still the most important. Do not put all your eggs in one basket, if you are not sure, it is better to rely on proven index funds.

Among the active threads

Combine stocks (growth) with bonds (stability), commodities (protection against inflation), and cash.

Between sectors

Technology companies do not own; add healthcare, energy, finance, and more.

Geographically

Invest globally (USA, Europe, emerging markets), not just in one country.

Regular inspection

Regularly monitor and adjust the composition of your portfolio to match your goals.

Three pillars of a real strategy

1. Yield ranking: Nobody has a crystal ball. Owning the "whole world" is the only proven way to always be there when something grows.

2. Rebalancing rule: Clean up your portfolio once a year. Sell part of the assets that have grown too much and buy what lags behind.

3. Own the engine of the world economy: When you invest in a broad index fund, you become a co-owner of thousands of real companies.

Investments in Horizon

The richest people in the world got rich by patience, not by speculation.

Market timing is more important than timing the market. Investment horizon is the period during which you plan to let your money work without withdrawing it. It is a key factor that determines how much risk you can afford:

📅 Short-term horizon (1 - 3 years)

You need money soon (e.g. for a wedding or a car). Here stability is important. We choose conservative tools where we do not risk a drop just when we need the money.

📊 Medium-term horizon (5 - 10 years)

Ideal time for a balanced portfolio. You can combine bonds with stocks. If the market drops for a year, you have time to wait for its recovery.

🚀 Long-term horizon (15+ years)

Your greatest ally. Over a horizon of more than 15 years, the historical risk of loss in the stock market approaches zero. Here, the power of compound interest is fully manifested - the longer the money "lies," the more interest works on interest.

Golden rule

The longer your horizon, the braver you can be. Time smooths out all temporary storms in the markets.

Time value: How much can you build with €100 per month?

This overview shows the fascinating difference between simply "saving" money and letting it grow through compound interest over time.

| Time horizon | Invested capital | 1% p.a. | 3% per annum. | 5% p.a. | 8% p.a. |

|---|---|---|---|---|---|

| 5 years | 6 000 € | 6 152 € | 6 465 € | 6 801 € | 7 348 € |

| 10 years | 12,000 € | 12 616 € | 13 974 € | 15 528 € | 18 295 € |

| 20 years | 24,000 € | 26 557 € | €32,830 | 41 103 € | 58 902 € |

| 30 years | 36,000 € | 41 964 € | €58,274 | €83,226 | 149 036 € |

| 40 years | €48,000 | 60 216 € | 92 606 € | 152 602 € | 349 101 € |

*Note: At 8% p.a. (which is the historical average of the world stock index), you can see that after 40 years you have more than 7 times what you actually put into the system.

Over the last 10 years (30th-40th year), the assets have grown by more than €200,000, even though you only invested another €12,000. That's the power of compound interest!

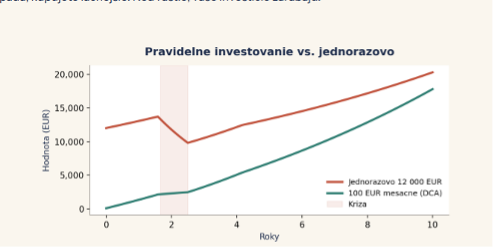

Regular vs Timing the market

If you missed only the 10 best days on the stock market in the last 20 years (which often come right after declines), your overall profit would be halved. If you missed the 30 best days, you would likely be at a loss.

Timing is not needed, you simply need to be on the market.

Trying to predict the movements of financial markets is as unpredictable as guessing numbers in roulette. Instead of fairy-tale profits, such investors usually end up with:

High costs

Frequent shopping and sales unnecessarily increase fees and taxes.

Missed opportunities

The best market growth days usually come just after the biggest drops.

Psychological stress

Constantly monitoring graphs and fear of mistakes lead to hasty emotional decisions.

Dollar-Cost Averaging (DCA)

Dollar-Cost Averaging (DCA) means investing the same amount at regular intervals — for example, 100 EUR per month. This strategy eliminates emotions and reduces the risk of bad timing.

When the market falls, you buy cheaper. When it grows, your investments earn.

Why does DCA work?

During a decline, you buy more shares for the same amount.

You don't have to guess when the "bottom" of the market is

Automation through a cron job = zero effort

Emotions do not get to decisions

What do the data tell us?

- • Short-term risk (1 year): If you try to "hit" the market and invest for only a year, it's almost like a lottery. You have up to a 27% chance of ending up with a loss because markets fluctuate up and down in the short term.

- • Power of patience (10 - 20 years): The longer you stay in the market, the closer the probability of profit gets to 100%. Over a 20-year horizon, history does not know of a case where an investor lost money.

Example of "The Worst Investor in the World"

Imagine an investor who invests only once a year, always on the worst possible day (just before a big crash). Even this investor will be profitable after 20 years if they do not withdraw the money. Regularity (DCA) beats bad luck and fear.

Active vs Passive Investing

WINNING STRATEGY

Why does less activity mean more money?

Many beginners think that successful investing requires hours of watching charts and "predicting" when prices will drop so they can buy advantageously. However, the reality is the opposite. The most profitable are those who do almost nothing.

Rule 90%

Active investing

Striving to select specific stocks (e.g. only Tesla or Apple) or trying to predict when the market will fall and when it will rise. The goal is to "beat the market".

Reality:

More than 90% of professional managers on Wall Street are unable to consistently beat the market's average growth. If experts with an army of analysts cannot do it, it is unlikely that an ordinary person in their spare time will succeed.

Passive investing

You are not buying one company, but the "whole market" (for example, through index ETF funds). You are not trying to be smarter than millions of other investors. You simply ride the wave of global economic growth.

Advantage:

Have a peaceful sleep, almost zero fees, and statistically a much higher chance of profit.

Delay cost

The biggest mistake is not choosing the wrong fund — it is waiting. Every year of delay costs you tens of thousands of euros.

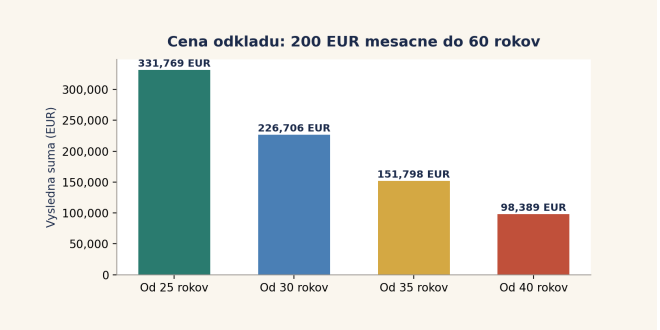

Look at the difference when you start investing 200 EUR per month at different ages:

When depositing €200 monthly

When depositing €200 monthly

When depositing €200 monthly

*the resulting amounts are based on an average annual yield of approximately 8% p.a. (which corresponds to the long-term historical average of the stock market).

Price of 10-year hesitation

If you start at 25, depositing €200 per month will result in a sum of approximately €331,000. If you start at 35, you will have only €151,000.

These 10 years of "waiting for the right moment" actually cost you €180,000. That's the value of one apartment you missed out on just because you were afraid to start.

The difference between starting at 25 and 40 years old is more than 233,000 EUR!

Time is your greatest ally. You don't have to start with large amounts - even 50 EUR per month is better than nothing.

"The best time to invest was ten years ago. The second best time is today."

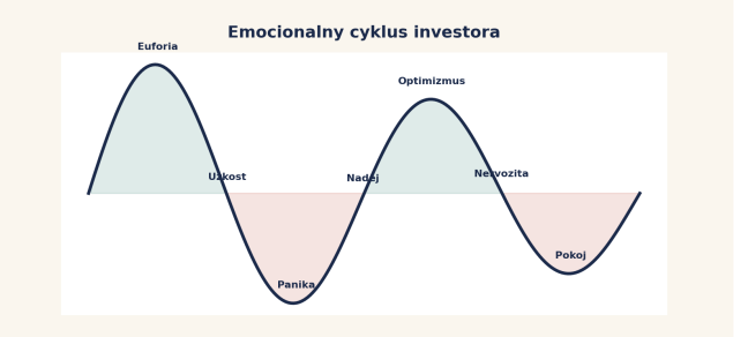

Investor Psychology

The biggest risk is not the market — it's your head. Investors make the worst decisions under the influence of fear and greed. Understand the emotional cycle and don't let it control your money.

Most common mistakes for beginners

• Investing without reserve

• Shopping at the top

• Portfolio review

• Striving to "hit bottom and peak"

• Investing based on emotions

• Inheriting "types" from friends

• Panic during declines and selling at the wrong time

Golden advice

When you see a 30% discount on shoes in a store, you run to buy them. When you see a 30% discount in the stock market (decline), most people run to sell.

The DCA strategy teaches to perceive declines as discounted purchases. The lower the market goes, the more shares you buy for your 100 EUR.

Before you start

Create a reservation

For example, 3-6 months of expenses

Clarify your goal

For example, retirement, financial freedom

Set the horizon and risk tolerance

Complete the investment questionnaire

Choose a simple core and regularity

Example 1 - 2 ETF and regular monthly deposit

Pre-start checklist:

I have a reserve or a plan on how to create it

I know what I am investing in and until when

I have chosen a regular contribution

Congratulations!

You have completed the Investment Academy.

Now you have all the knowledge needed to start your investment journey.